THE GLENIGAN FORECAST 2020 – 2022

Construction & COVID-19 – How will the construction industry recover?

The COVID-19 pandemic and the lockdown of much of the UK economy from late March have inflicted a massive external shock to UK construction.

Added to that, the threat of the worst recession in living memory, is obviously causing major concerns for every business working in and around the construction industry at this time.

But all is not lost, and some comfort can be taken from the Government’s focus on the construction industry to help drive a recovery from the post-pandemic shock and the recession.

It’s reassuring that the Government is focusing it’s recovery plans on infrastructure investment, which will not only aid the industry, but the wider economy too.

The Glenigan Construction Industry Forecast for 2020 – 2022 details which sectors will benefit from strong investment and future work pipelines, as well as identifying where risks are most prevalent over the forecast period.

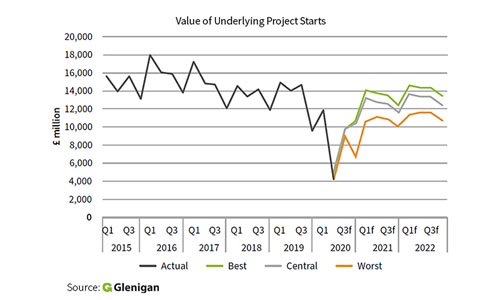

Although, the value of underlying project starts fell by an estimated 62% during the second quarter, a sharp rebound in construction output and project starts is forecast for the third quarter following the lifting of lockdown restrictions. A more gradual, but sustained recovery is anticipated for the remainder of the forecast period. By 2022, the value of underlying project starts is forecast to total £52.4 billion, just 1% below 2019 levels.

Sector Focus

A weak UK economy is expected to constrain construction activity over the forecast period, with private sector workload particularly weak.

Value of Underlying Project Starts by Sector

Manufacturing

UK manufacturing faces weak domestic and overseas demand. In addition, UK manufacturers have less favourable access to the EU single market and potential disruption to EU sourced supply chains from next year.

However, if anything good can be taken from the COVID-19 pandemic, it is that contractors have had to shore up their UK supply chain to keep jobs working, and therefore should be in a slightly better position to cope with the challenges ahead once we do leave the EU.

Against this background we anticipate a continued weakening in manufacturing investment over the forecast period.

Warehousing & Logistics fair much better

In contrast, warehousing & logistics premises are forecast to remain a growth area, bolstered by long-term growth in online retailing which is driving the demand for logistics space. Although growth in this area has been disrupted in the short term by the lockdown, warehousing and logistics activity is forecast to grow strongly during 2021 and 2022.

Decline in retail sector activity

In the retail sector, activity is forecast to decline over the forecast period as weak consumer spending and the growth in online retailing accelerate the restructuring of the retail industry and depress the demand for retail premises.

Turbulent time for Offices

Office starts are forecast to decline sharply this year as the lockdown exacerbates a cyclical downturn in sector activity. Project starts are forecast to recover during 2021 and 2022, supported by a rise in refurbishment projects as tenants and landlords adapt premises to accommodate changing working practices. New-build office projects are likely to be slower to recover, as tenants and developers assess the impact of rising unemployment and the potential structural shift in remote working on the long term demand for office accommodation.

Private Housing suffers

The COVID-19 pandemic has hit private housing activity hard. As suspended sites are re-opened, housebuilders are prioritising sites that are close to completion. With home-buyers confidence dented by the poorer economic outlook, the recovery in project starts is expected to be gradual over the forecast period.

Increased Government Investment

Social housing to bounce back

Social housing activity picked up during 2019. While the pandemic has caused a short-term hiatus in starts this year, renewed growth is anticipated from 2021.

In contrast, student accommodation work faltered during 2019 and a further marked contraction in student accommodation work is expected this year, with only a limited recovery in this sub-sector during 2021 and 2022.

Schools to outperform Universities

An increase in school building projects is forecast to drive a recovery in sector activity during 2021 and 2022 as local authorities tackle a shortage of secondary school places. A fall in universities capital spending is expected to temper the overall growth in education sector work.

Growth for the Health Sector

The outlook for the health sector is brightening, with promised increases in NHS capital funding expected to lift project-starts over the next two years. The Nightingale temporary hospital programme has bolstered project starts this year. Starts are subsequently forecast to gather momentum during 2021, rising by 27%, as NHS trusts develop and implement their investment programmes.

Strong recovery for Civil Engineering sector

While civil engineering project starts, along with other sectors, have been disrupted and delayed by the lockdown, the sector is set to recover strongly over the forecast period. The government has pledged to significantly increase investment in the UK’s infrastructure with the Prime Ministers Build, Build, Build announcement on 30th June. In many areas such as energy and broadband, such investment will be delivered by the private sector.

Where additional public sector funding is potentially available in areas such as roads, it may take time before additional projects are ‘shovel-ready’. Therefore, we anticipate that initially, additional funding will be directed at areas such as tackling the maintenance backlog on the nation’s roads.

Existing major infrastructure schemes, including Thames Tideway, HS2 and Hinckley Point, are also forecast to lift civil engineering output over the forecast period. The £1.4 billion Stonehenge Tunnel is currently scheduled to start in 2021, but important planning and contracting hurdles have yet to be cleared.

Leave a Reply

Want to join the discussion?Feel free to contribute!