Building News is an information portal for all professional building specifiers. Here you can find all of the latest construction news from around the UK and the rest of the world.

Rinnai’s CPD, ‘Seasonal Performance Factors and Heat Pump Design’, details the evaluation of SPF when measuring a heat pump system’s overall energy efficiency throughout an entire heating season, whilst further considering variations in temperature and other system factors.

Rinnai’s Seasonal Performance Factors and Heat Pump Design CPD details the potential limitations of manufacturer-issued efficiency measures for Heat pumps, namely COP (Coefficient of Performance) and SCOP (Seasonal Coefficient of Performance). Manufacturers often measure heat pump efficiency using Coefficient of Performance (COP), which is the ratio of useful heat energy produced to the electricity consumed at a specific external air temperature.

A SCOP efficiency rating solely measures the heat pump unit which may yield a lack of system congruity when considering the entire system. Consequently, relying on this performance measurement alone can affect customer expectations in system performance and carbon reductions.

Rinnai offer an alternative methodology in measuring system efficiency; a Seasonal Performance Factor approach evaluates all energy utilizing components within a commercial hot water system and measures the performance of the entire system, as opposed to solely the heat pump.

By presenting this CPD to UK customers, contractors, consultants, specifiers and installers, Rinnai aims to provide information that delivers a concise and true account of commercial hot water heating performance using the ‘Seasonal Performance Factor’ methodology.

Rinnai UK’s new division – Rinnai Applied has multiple bursaries available and to qualify you must be fully eligible and successfully complete the three CPD sessions between now and March 2026.

The CPDs are on the following subjects:

Seasonal Performance Factors (SPF) and Heat Pump Design

Introduction to Water Neutrality

Retrofitting Heat Pumps into the Leisure Sector through CCA & SPF Analysis

Rinnai continues to inform the UK market of system operating details that provide an accurate statement of performance, while considering the effects on operational expenditure, economic investment, and environmental impact.

RINNAI OFFERS CLEAR PATHWAYS TO LOWER CARBON AND DECARBONISATION

PLUS CUSTOMER COST REDUCTIONS FOR COMMERCIAL, DOMESTIC

Rinnai’s range of decarbonising products – H1/H2/H3 – consists of hot water heating units in gas/BioLPG/DME, hydrogen ready units, electric instantaneous hot water heaters, electric storage cylinders and buffer vessels, a comprehensive range of heat pumps, solar, hydrogen-ready or natural gas in any configuration of hybrid formats for either residential or commercial applications. Rinnai’s H1/2/3 range of products and systems offer contractors, consultants, and end users a range of efficient, robust, and affordable low carbon/decarbonising appliances which create practical, economic, and technically feasible solutions.

Rinnai is a world leading manufacturer of hot water heaters and produces over two million units a year, operating on each of the five continents. The brand has gained an established reputation for producing products that offer high performance, cost efficiency and extended working lives.

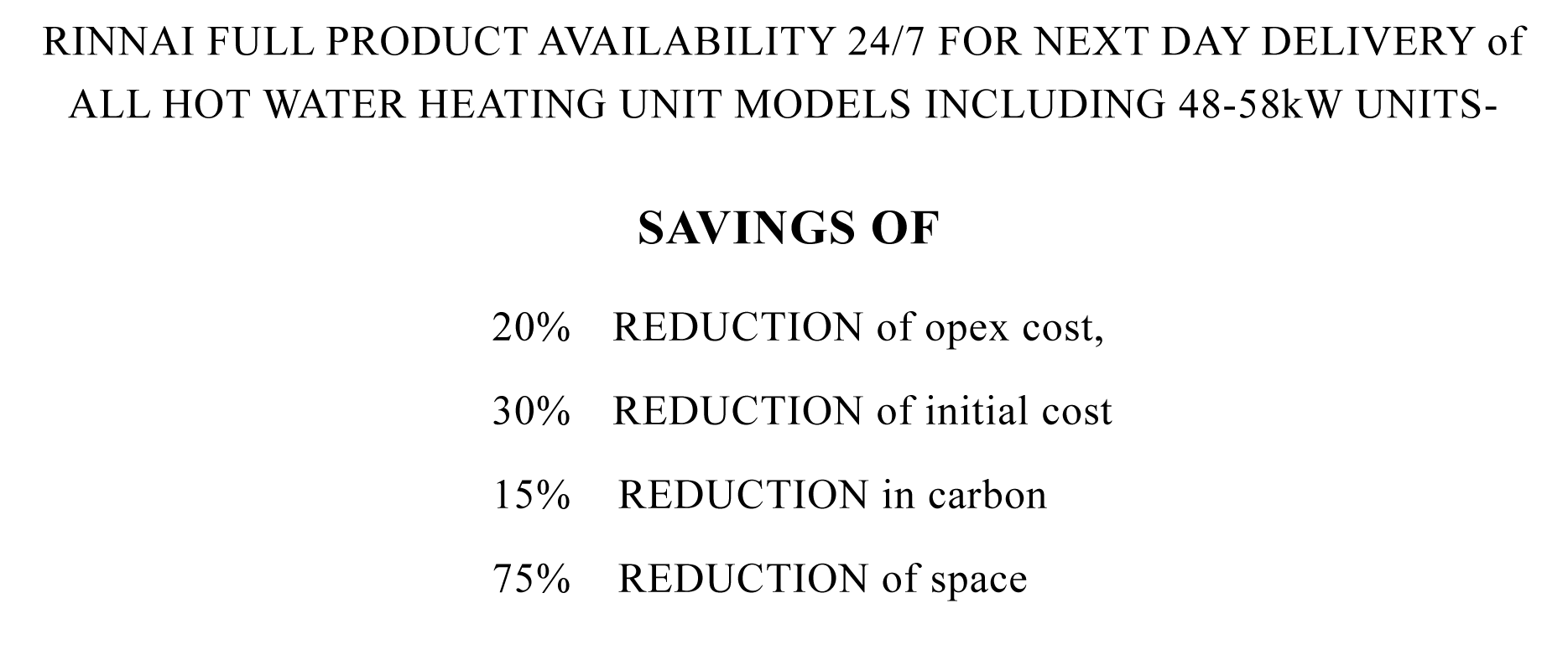

Rinnai products are UKCA certified, A-rated water efficiency, accessed through multiple fuel options and are available for purchase 24/7, 365 days a year. Any unit can be delivered to any UK site within 24 hours.

Rinnai offer carbon and cost comparison services that will calculate financial, and carbon savings made when investing in a Rinnai system. Rinnai also provide a system design service that will suggest an appropriate system for the property in question.

Rinnai offer comprehensive training courses and technical support in all aspects of the water heating industry including detailed CPD’s.

The Rinnai range covers all forms of fuels and appliances currently available – electric, gas, hydrogen, BioLPG, DME solar thermal, low GWP heat pumps and electric water heaters More information can be found on Rinnai’s website and its “Help Me Choose” webpage.

https://buildingspecifier.com/wp-content/uploads/2025/11/rinnai-na-19.11.25.jpg320800Lynhttps://buildingspecifier.com/wp-content/uploads/2019/06/building-specifier-logo.pngLyn2025-11-18 11:52:442025-11-18 11:52:44Understand SPF for Smarter Heat Pump System Design with Rinnai CPD

Free Access for Industry Professionals – and Learn & Earn Bursaries

Rinnai’s recent additions to the company’s extensive list of industry relevant CPDs include SPF – Seasonal Performance Factors and Heat Pump Design; Introduction to Water Neutrality and Retrofitting Heat Pumps into the Leisure Sector through CCA & SPF Analysis.

Sign up today as places are limited at and see how you can earn and learn bursaries of up to £200 on successful completion of all three CPDs.

All the CPDs provide updated insights into significant issues concerning contractors, consultants, specifiers, system designers, and installers operating in the UK HVAC market.

A CPD on Seasonal Performance Factor (SPF) discusses the measure of a heat pump system’s overall energy efficiency over an entire heating season, considering variations in temperature and other system factors. This CPD helps with assessing the real-life performance of a heat pump system when in use.

A CPD on Water Neutrality details a subject that will become increasingly important as UK water supplies become less accessible due to overpopulation and climate change. Rinnai aims to increase awareness of this issue as well as supply industry insight into the question: should water neutrality be added to national legislation?

A CPD on Heat Pumps Retrofit evaluates all aspects of this increasingly important subject. Heat Pumps can be readily fitted to existing or even older properties in both residential and commercial sectors. This CPD analyses the specific needs of retrofitting in terms of design, appliance installation as well as meeting the required heating and hot water demand. Further attention is applied to how the concept of retrofitting demands further attention in relation to maximising energy efficiency.

All Rinnai CPDs are CIBSE accredited. Rinnai Applied supports a transparent and educational approach to information sharing that provides specifiers, system designers, contractors, installers, and customers with nutritional knowledge that adds understanding and clarity towards evolving ideas inside the UK HVAC industry.

Rinnai UK’s new division – Rinnai Applied – is also offering an opportunity to gain bursaries of £200 when those eligible successfully complete these three specific CPDs.

Rinnai continues to inform the UK market of system operating details that provide an accurate statement of system performance, while considering the effects on operational expenditure, economic investment, and environmental impact.

Sign up today as places are limited

RINNAI OFFERS CLEAR PATHWAYS TO LOWER CARBON AND DECARBONISATION

PLUS CUSTOMER COST REDUCTIONS FOR COMMERCIAL, DOMESTIC

Rinnai’s range of decarbonising products – H1/H2/H3 – consists of hot water heating units in gas/BioLPG/DME, hydrogen ready units, electric instantaneous hot water heaters, electric storage cylinders and buffer vessels, a comprehensive range of heat pumps, solar, hydrogen-ready or natural gas in any configuration of hybrid formats for either residential or commercial applications. Rinnai’s H1/2/3 range of products and systems offer contractors, consultants, and end users a range of efficient, robust, and affordable low carbon/decarbonising appliances which create practical, economic, and technically feasible solutions.

Rinnai is a world leading manufacturer of hot water heaters and produces over two million units a year, operating on each of the five continents. The brand has gained an established reputation for producing products that offer high performance, cost efficiency and extended working lives.

Rinnai products are UKCA certified, A-rated water efficiency, accessed through multiple fuel options and are available for purchase 24/7, 365 days a year. Any unit can be delivered to any UK site within 24 hours.

Rinnai offer carbon and cost comparison services that will calculate financial, and carbon savings made when investing in a Rinnai system. Rinnai also provide a system design service that will suggest an appropriate system for the property in question.

Rinnai offer comprehensive training courses and technical support in all aspects of the water heating industry including detailed CPD’s.

The Rinnai range covers all forms of fuels and appliances currently available – electric, gas, hydrogen, BioLPG, DME solar thermal, low GWP heat pumps and electric water heaters More information can be found on Rinnai’s website and its “Help Me Choose” webpage.

ACV UK Expands CIBSE-Approved CPD Portfolio with New Module on Commercial DHW Systems

ACV UK, a leading specialist in hot water and heating solutions, has expanded its CIBSE-approved CPD portfolio with the launch of a new module: “What You Need to Know – Commercial DHW Systems Now and for the Future”. Designed for building services professionals, the new CPD helps consultants, specifiers and contractors navigate the fast-moving landscape of domestic hot water (DHW) system design in commercial buildings.

With the need to comply with updated regulations and improve system efficiency, the new CPD from ACV UK explores how market demands are shifting and what that means for modern DHW system specification. It also covers key drivers such as changes to Part L, the expanding range of available technologies and how to approach system design in a way that balances carbon reduction, reliability and cost. Participants will also gain insights into demand profiling, system sizing, hybrid strategies and practical considerations such as site constraints and long-term operational performance.

Designed for professionals involved in new build projects, plant room upgrades, or refurbishment work, the session provides a clear, practical overview of both the challenges and opportunities shaping the future of commercial DHW. To suit busy working schedules, the CPD lasts 45–60 minutes and can be delivered in person, online, or at ACV’s Expert Academy Training Centres.

The new module complements ACV UK’s existing portfolio of CIBSE-approved CPDs. These include “Factors Driving Material Selection for Hot Water Storage Products” which highlights the durability and performance of stainless steel in commercial DHW systems, and “Decarbonisation Using Electric Boiler Technology in Non-Domestic Properties,” which examines how electric boilers can support carbon reduction goals, particularly in hybrid systems or installations where heat pumps are not feasible.

As the industry continues to adapt to the net zero agenda and increasingly complex regulatory requirements, ACV’s CIBSE-approved CPD programme equips professionals with the knowledge needed to deliver quality, future-proof solutions.

https://buildingspecifier.com/wp-content/uploads/2025/10/AVC-30.10.25.jpg320800Lynhttps://buildingspecifier.com/wp-content/uploads/2019/06/building-specifier-logo.pngLyn2025-10-29 12:17:022025-10-29 12:17:02New Module on Commercial DHW Systems from AVC UK

Groundforce Shorco has supplied a variety of specialised props and beams to support a complex deep excavation in the centre of London.

Specialist contractor Ground Construction Ltd was employed by main contractor Ardmore to carry out extensive basement works for a new life science campus in the King’s Cross Knowledge Quarter.

Designed by architects Bennett Associates for developer the Reef Group, the Tribeca development will ultimately provide a million square feet of life sciences, office, retail, leisure and residential space.

Phase One was completed in July 2024 and Ardmore’s £240m contract for Phase Two – comprising three multi-storey buildings totalling 540,000 sq ft – is due for completion in 2026.

Ground Construction Ltd used Groundforce temporary propping equipment to support the main basement excavation for Blocks C2 and C3 as well as multiple smaller excavations within the main excavation area.

Due to the complexity of excavation, a variety of propping equipment was required, ranging from light-duty MP30 mechanical struts to the MP375, one of the largest in the Groundforce Shorco range of modular hydraulic struts, capable of supporting a load of 375 tonnes.

Groundforce Mega and Super Mega Brace waling beams were employed to transfer the lateral loads to the contiguous bore piles and steel sheet piles lining the sides of the excavations.

The excavations ranged in depth from about 8.5m in Block C2 to as much as 15m in the main excavation area, and ranged in width from about 2.5m to 44m.

A total of 28 Groundforce Shorco props have been installed on the project. Nine MP250s and the one MP375 were installed within the main excavation; four MP150s were installed to support the retaining wall in the southwest excavation; 13 MP150s, two MP30s and one MP250 support the excavation for the attenuation tank, and four MP250s were located in the core cap excavation.

Groundforce Shorco’s ability to mix-and-match components from its range of modular components was essential to providing a tailored solution to this complex task. In addition to the four different sizes of prop, they also supplied extension tubes in diameters of 508mm, 610mm, 813mm and 1,220mm (the largest in the range) to ensure the optimum combination of strength, stiffness and compactness.

The largest tubes – the 1,220mm Super Tube – were used in combination with MP250 hydraulic rams to span the 44m width of the main excavation at two levels.

The site’s location in a densely populated urban area provided an additional challenge for the site team.

“The site has roads on two sides and a canal along a third,” says Ground Construction Ltd Temporary Works Director Keith O’Connor.

Load monitoring has been used for some of the props in the main excavation along the run to ensure that loadings are closely monitored for any increases beyond the design limits.

The excavation is complicated and has been tricky, admits Keith. “But the biggest challenge has been managing the sequence of the works and the release of areas on site,” he says.

“There were a number of Interacting excavations which required careful management across the site but we worked with GCL to ensure safe, efficient and adaptable solutions. Contributing to such a landmark London development and seeing our designs perform on site has been highly rewarding,” says Hussein Koussan, Design Engineer at Groundforce Shorco.

Ground Construction Ltd and Groundforce Shorco have worked together on several previous projects and teamwork has been crucial on this site, says Keith O’Connor:

“This has been a challenging project but progress has been quite straightforward.”

The Pallet LOOP enhances offer with three-day collection service

Ten-day service replaced by faster solution to support waste and sustainability goals

Companies using The Pallet LOOP across the UK mainland will now get their pallets picked up faster, as the business introduces a free three-day collection service option.

With immediate effect, all collections booked via The Pallet LOOP’s nationwide recovery network will be completed within three working days – reflecting The Pallet LOOP’s dedication to customer service, supply chain efficiency, and environmental responsibility.

Through this groundbreaking scheme, businesses earn £2 to £4 for every LOOP pallet that is returned, ensuring they are continually reused, while also reducing construction waste.

Part of timber and forestry business BSW Group, The Pallet LOOP previously offered two collection possibilities; a three-day service (with a £100 fee); and a free ten-day option.

LOOP’s free three-day service now becomes the default, replacing the current ten-day offer. Simplifying the collection service will support the UK construction industry in several ways:

Reduced storage requirements: Shortening the LOOP collections window to three days will help pallet recipients free up valuable yard, site and warehouse space.

Enhanced sustainability: With a faster collections service, more LOOP pallets re-enter the supply chain more quickly, rather than ending up damaged or in skips.

Greater customer satisfaction: The speed of collections has been a consistent topic in customer feedback received by The Pallet LOOP, particularly from site managers in large cities, where there is limited space to store pallets.

Andy Williamson, Managing Director of The Pallet LOOP, said:

“Offering a prompt collection service is another critical step to closing the loop on pallet waste and delivering on our circular economy model.

“No one wants to see LOOP pallets laying around, taking up valuable space. By guaranteeing collection within three business days, we’re making life easier for customers and ensuring pallets get back into circulation where they belong, as quickly as possible.

“It’s an operational shift that shows us stepping up a gear, which is ultimately a win for the circular economy, building materials supply chain and the environment.”

With The Pallet LOOP’s three-day service, the collection of 50 or more pallets (green and white) is free, but collections of under 50 pallets will incur a £100 charge, while each standard white pallet returned will also cost £2.

“They’re Building Houses From Dirt Now”: Japan’s Revolutionary Discovery That Changes Construction Forever

In a groundbreaking move that could redefine sustainable construction, Japanese company Lib Work is utilizing 3D printing technology to build homes using earth instead of traditional concrete, offering a glimpse into the future of eco-friendly architecture.

In recent years, 3D printing has made significant strides in the construction industry, with innovative projects sprouting up around the globe. From rapid construction homes in Portugal to the architectural marvel of the 6,500-square-foot Wavehouse in Germany, the technology is reshaping how we think about building. Now, a Japanese company called Lib Work is pushing the boundaries of sustainability in 3D printing by using earth instead of concrete as a primary building material. Their prototype, the Lib Earth House, stands as a testament to what can be achieved when tradition and technology intersect in novel ways.

Saying Goodbye to Concrete: Embracing Earth

While Lib Work is not the first to explore 3D printing in construction, it distinguishes itself by completely eliminating concrete from its building process. Traditionally, concrete has been a staple in 3D printed structures, especially for foundations. However, Lib Work has opted for a combination of earth, lime, and natural fibers, even for the foundation. This innovative approach has resulted in a single-story home with an area of approximately 1,100 square feet. The company’s decision to forgo concrete is not merely symbolic; they have also developed technology to ensure that their unique material mix possesses adequate strength and workability for construction purposes.

Lib Earth House Model B: Key Features

The creation of the Lib Earth House involved collaboration between Lib Work Co., Arup, and Wasp, the manufacturer of the 3D printer used. The house’s standout feature is its recyclability at the end of its lifecycle. Key elements include:

Component

Description

Foundations and Walls

Earth-based mixture

Structure

Wooden frame

Rooms

Living/dining area, bathroom, kitchen, toilet

Exterior Environment

Court with natural space

Technology

Tesla Powerwall battery + solar panels

Style

Modern

The use of renewable energy sources like solar panels and Tesla’s Powerwall battery further underscores the project’s commitment to sustainability. The modern design is not just an aesthetic choice but a statement about the future of eco-friendly living.

The Future of Construction and Lib Work

3D printing in construction offers numerous advantages, including rapid execution, cost-effectiveness, and efficient material usage. This method significantly reduces environmental impact, whether using concrete or earth. For Lib Work, the ability of 3D technology to create shapes that are otherwise impossible to construct opens doors for extreme customization. This is not limited to residential homes but extends to other types of buildings as well. The company is eyeing future projects that could even involve construction on Mars, illustrating their far-reaching vision.

Challenges and Opportunities in Sustainable Construction

The shift from traditional materials like concrete to more sustainable options such as earth involves several challenges. Ensuring the structural integrity and durability of earth-based materials is a primary concern. However, as technology advances, these challenges are being met with innovative solutions. Lib Work’s approach could inspire other companies to explore similar sustainable practices. The construction industry is at a pivotal point where environmental considerations cannot be ignored. As companies like Lib Work demonstrate the potential of earth-based 3D printing, the industry could see a broader adoption of these methods.

The journey towards sustainable construction is not without its hurdles, but the opportunities for reducing environmental impact and enhancing living conditions are immense.

As we look to the future, the question remains: How will the integration of sustainable materials and advanced technologies shape the next generation of construction practices? The potential for change is significant, and the direction we choose could redefine the built environment for years to come.

https://buildingspecifier.com/wp-content/uploads/2025/09/BSC-27.09.25-5.jpg320800Lynhttps://buildingspecifier.com/wp-content/uploads/2019/06/building-specifier-logo.pngLyn2025-09-27 08:38:522025-09-27 08:38:52‘They’re Building Houses From Dirt Now’

The race to build AI infrastructure is on and speed is everything

Amid the challenges now synonymous with building AI infrastructure, stakeholders still expect data centers on demand. So, what are the best strategies for delivering next-gen facilities, fast?

The rapid evolution of AI is reshaping industries and data centers are at the epicenter of that change. AI has transformed how we design, build, and operate these facilities. It is driving demand for new infrastructure centers built to handle high-density workloads, designed with scalability at their core.

This urgency is further compounded by complex supply chain issues, including shortages of critical components, extended lead times, and rising material and transportation costs. At the same time, labor and knowledge gaps, plus mounting demand for power to support energy-hungry applications, present layers of challenges.

In this high-pressure landscape, Exyte supports operators with strategies built for speed, scale, and reliability. As a global leader in end-to-end infrastructure solutions, Exyte draws on deep technical experience, strong vendor relationships, and modular construction expertise.

Axel Favillier, director project & construction management data centers at Exyte, explains how a manufacturing mindset and early engagement are key to staying ahead of supply chain volatility and rising technical demands. Even amid uncertainty, Exyte’s strategy enables clients to move quickly, reduce risk, and compete at scale.

Getting ahead of the supply chain

Volatility in the global supply chain has become a familiar challenge, as geopolitical factors and material shortages regularly disrupt access to essential components and systems. For data centers, these disruptions are threatening project timelines and budgets.

To stay ahead, Exyte prioritizes early and proactive involvement in the procurement process. By engaging at the design stage and promptly securing orders for essential equipment, Exyte can minimize the risk of delays and enhance the resilience of project schedules.

According to Favillier, “This approach keeps projects moving and ensures teams are ready to pivot when challenges arise.” At the same time, the company incorporates mitigation strategies into its project plans, allowing teams to swiftly adapt if supply issues arise.

Early engagement supports a modular construction approach, where components are designed, fabricated, and tested off site before being delivered and installed on site. By participating early in the engineering and procurement process, teams can align design decisions with manufacturing capabilities resulting in faster assembly, improved quality control, and greater efficiency on site.

A manufacturing mindset

With a growing network of offsite prefabrication facilities, Exyte manufactures its own core modules including electrical, mechanical, and integrated systems under controlled conditions. This not only improves quality and consistency but also reduces onsite labor requirements and construction risks.

Exyte continues to invest in its in-house engineering and manufacturing capabilities to deliver high-performance, future-ready infrastructure solutions as standard. “The expectation in the near future is for an aggressive increase in the proportion of our buildings to be built off-location on satellite sites, modules built in factories and brought to location,” says Favillier.

“When we modularize, we operate with a manufacturing mindset. We are tracking timelines closely, anticipating issues thanks to lean production management, and addressing these issues before they happen to help keep timelines on track.”

Controlling the end-to-end process from procurement through installation and de-risking delivery is a pivotal advantage. This approach to supply chain management helps ensure Exyte can deliver AI-ready infrastructure at pace, transforming uncertainty into a confident commitment that clients can rely on.

Providing built-in flexibility

As AI adoption accelerates, so is the pace of change within every aspect of the data center. Today’s workloads are more power and cooling intensive than ever before, and facilities must be designed to evolve alongside demand. As such, flexibility is a mission-critical priority.

From layout to mechanical systems, built-in flexibility allows operators to adapt to changing demands without major disruptions to the infrastructure. Modular construction supports this agility by allowing large elements of the data center to be pre-assembled and delivered as complete units, ready to go as soon as they arrive on site.

One of the most pressing examples of the need for flexibility is cooling. As data centers transition from traditional air cooled systems to liquid or hybrid methods, many legacy facilities are proving difficult to retrofit. New designs must not only support today’s workloads but anticipate tomorrow’s requirements.

Exyte is addressing this by making modularity the foundation of its designs: “We are consistently looking at smart ways to modularize data centers, not just for specific components, but for the entire structure,” says Favillier.

“That way, when clients need to increase their power or cooling capacity, they can scale by simply adding another module set. This is all designed to be stacked, expanded, and upgraded like Lego blocks.”

Balancing standardization with customization is also key. By standardizing core modules and processes, Exyte creates efficiencies across quality control, assembly, safety, and installation. This reduces rework, enhances consistency, and accelerates project timelines, while allowing operators to tailor layouts and performance features to meet specific business needs.

Quality control is another core benefit of this approach. By manufacturing modules in controlled environments, inspections and quality tests can be conducted before components ever arrive on site.

Once delivered, these plug-and-play systems are connected, tested, and commissioned with minimal disruption. The result is a faster, more predictable construction timeline and a data center built to perform from day one and fit to scale up in the future.

The value of a global footprint

In a supply-constrained and highly specialized industry, global reach offers a significant strategic advantage. With operations across strategic markets, Exyte can tap into a broader network to source materials and components, manage regional cost fluctuations, and deploy expert teams on the ground wherever they are needed.

A global footprint also enables a consistent approach to project delivery, regardless of location. Exyte prioritizes standardization across engineering, construction, and project management so that each and every project reflects the company’s commitment to quality, safety, and innovation.

This consistency in approach provides a level of predictability where customers know what to expect, whether building in Asia, Europe, or North America. For companies expanding into new geographies, having a trusted partner that can replicate a successful model across borders is invaluable.

The ability to deploy local expertise on a global scale throughout each stage of a project, means the company can track progress in real-time, identify bottlenecks early, and keep projects moving forward.

From design through to delivery, this boots-on-the-ground model helps enforce global best practices for health and safety, ensuring that even in local markets, projects meet international standards, and every undertaking is delivered with safety as a top priority.

Leveraging vendor relationships

Soaring demands bring expanding supply chains. The industry is experiencing a rush of new entrants – namely vendors and service providers looking to capitalize on growth. While this has sparked innovation, it’s also made reliability and consistency harder to guarantee.

To maintain control and reduce risk, Exyte emphasizes two strategic approaches: building internal capabilities and developing strong trade partnerships. On the self-sufficiency side, the company is increasingly taking responsibility for scopes traditionally handled by subcontractors, such as having its own in-house module manufacturing capabilities allowing it to better manage project timelines, costs, and safety standards.

Equally, Exyte recognizes the value of strategic partnerships working to shift from transactional relationships to long-term collaborations and evolving from subcontractor roles to trade partner mindsets.

“We are looking to bring our partners along with us,” explains Favillier. “It’s about developing mutual trust and raising standards together, over time, especially as we grow into new regions.”

This includes blending global suppliers with local contractors. International vendors bring scale and consistency, while local partners contribute essential knowledge of building codes, labor regulations, and health and safety practices specific to the region. Together, these partnerships enable Exyte to maintain consistently high standards while adapting to local nuances.

It’s clear that, in today’s uncertain landscape, where geopolitical tensions and economic volatility can cause ripple effects across global supply chains, having a clear strategy and the right partners is essential.

AI has ushered in a new generation of complex challenges, as well as exciting opportunities. Facilities must be built faster, perform better, and possess the capacity to evolve continuously. In this environment, combining speed with foresight and flexibility is foundational to long-term success.

Exyte is helping operators meet demand and overcome primary obstacles with an approach rooted in innovation, forward-thinking, and strategic collaboration. Through modular design, global reach, early procurement, and strong partnerships, Exyte is well-equipped to deliver the AI-ready infrastructure of tomorrow, today.

https://buildingspecifier.com/wp-content/uploads/2025/09/BSC-27.09.25-2-1.jpg320800Lynhttps://buildingspecifier.com/wp-content/uploads/2019/06/building-specifier-logo.pngLyn2025-09-27 07:24:262025-09-27 07:24:26The race to build AI infrastructure

UK ventilation manufacturer Nuaire will proudly be displaying its sustainability credentials at this year’s UK Construction Week at the NEC, Birmingham, 30th September – 2nd October, on stand D71.

With increasing emphasis being placed on reducing embodied carbon within mechanical, electrical, and plumbing (MEP) systems – which are estimated to account for around 23% of a building’s embodied carbon – Nuaire is leading the ventilation industry in its drive to substitute high carbon materials with more sustainable alternatives, without compromising performance, reliability, or indoor air quality.

Nuaire is the first UK ventilation manufacturer to switch to recycled and renewably produced XCarb® steel across its BPS air handling units and XBOXER XBC packaged heat recovery systems, the latter of which will be on display at UK Construction Week. This shift will result in a 64% reduction on the steel proportion of Nuaire’s SCOPE 3 embodied carbon activity within the first year alone, compared with the same steel manufactured via the conventional steelmaking route.

Similarly, plastics used in residential ventilation systems and ducting often rely on virgin fossil-based polymers. Nuaire has changed to recycled plastic for its ducting, which will also be displayed at the show, along with Ductmaster Thermal all-in-one thermal ducting solution Nuaire’s metal air brick range for use in high-rise residential buildings.

In line with the sustainability theme of Nuaire’s stand at this year’s UK Construction Week, the latest evolution in Nuaire’s Drimaster-Eco Positive Input Ventilation (PIV) unit will be revealed. Highly effective at preventing condensation dampness, PIV technology was invented by Nuaire over 50 years ago, and continues to be developed for greater efficiency and sustainability. With Awaabs Law coming into force on the 27th October in the social rented sector, and being extended to the private rental sector, Drimaster remains a highly effective solution for landlords to prevent damp and mould.

Of course, ventilation doesn’t just protect against damp and mould, it is effective in addressing overheating, a more modern day issue to be found in many urban high-rise new builds. Nuaire will be showing its Hybrid Cooling System at UK Construction Week, which has been designed to tackle residential overheating in properties where window openings are limited and insufficient to naturally ventilate excess heat. The Nuaire Hybrid Cooling unit works in tandem with its MRXBOX MVHR. It activates when indoor temperatures exceed a threshold—typically 23°C—and introduces pre-cooled fresh air to help maintain occupant comfort.

Also on display at this year’s UK Construction Week will be Nuaire’s Faith-Plus from decentralised mechanical extract ventilation (dMEV) fan, designed to provide Building Regulations compliant continuous background extract ventilation for social housing.

Providing customers with a true breadth of ventilation solutions and expertise, whether it be the residential new build sector, social housing or commercial applications, Nuaire ventilation systems are renowned for saving energy and improving indoor air quality.

Nuaire is part of the Genuit Group of businesses which serve the construction industry.

https://buildingspecifier.com/wp-content/uploads/2025/09/NUAIRE2-25.09.25.jpg320800Lynhttps://buildingspecifier.com/wp-content/uploads/2019/06/building-specifier-logo.pngLyn2025-09-24 11:40:462025-09-24 11:40:46Nuaire puts sustainability at the fore at UK Construction Week, Birmingham

A dilapidated railway station building has been brought back from the brink of dereliction with a little help from Welsh Slate.

Some 16,000 of the leading UK manufacturer’s 500mm x 300mm Ffestiniog Blue Grey Capital-grade slates now adorn the roof of the historic Grade II listed Cambrian Railways Building in the market town of Oswestry on the Shropshire/Welsh border.

It has been three years since the building has been properly visible as it was shrouded in scaffolding following storm damage in 2022 when a number of eaves corbels became loose. These are specifically referenced in the Listing by Historic England and are a key feature of the building.

Funded by the UK Shared Prosperity Fund and owners Shropshire Council, this £630,000 phase of the renovation scheme has been completed in nine months by local building conservation specialists Phillips and Curry in conjunction with consulting architectural technicians Donal Insall, Cambrian Heritage Railways, Oswestry Town Council and the Future Oswestry Group.

Work has included removing dangerous asbestos roof tiles and replacing them with 750m2 of the ones from Welsh Slate’s Ffestiniog quarry, and restoring the building’s exterior to prevent falling masonry, as well as giving windows and doors a fresh coat of Cambrian Railway colours.

The scheme has also included installing nesting boxes for swifts under the eaves as well as bat roosting tiles along the roof which features six large chimneys and multiple hips and valleys. The Ffestiniog slates were graded into four thicknesses by Philips and Curry before they were laid and fixed with large-headed copper clouts.

Due to the tight site, Philips and Curry installed a haki scaffold stair to improve roof access for site operatives, along with a rack and pinion goods hoist to safely lift all materials to roof level.

The Cambrian Station Building boasts a rich history that stretches back to the mid-1860s. Once serving as the local railway station and the Cambrian Railway headquarters, it was key in connecting Oswestry and North Wales. Though still used seasonally by the Cambrian Heritage Railway, the building needed major investment to stay safe and functional.

Shropshire Council’s property management arm, Property Services Group (PSG), found the original Victorian roof, which would have been Welsh Slate from the quarries served by the Cambrian Railway, required significant repair and restoration.

A report by the council’s Historic Environments team identified several areas of “large-scale damage” caused by rainwater from the leaking roof, along with what they described as “the combined effect of material saturation, construction defect, inappropriate intervention and poor maintenance.”

Significant renovations had been made in the 1970s but these included the replacement of the original Welsh slates with a ceramic composite tile which contained asbestos, and the removal of many of the building’s architectural features.

It was originally thought it would be possible to save most of the nearly 300 existing eaves corbels by just replacing the worst of the delaminating and loose ones, but after thorough testing and trialling on site, it was decided longevity of repair could not be guaranteed.

Shropshire Council sought building consent and instructed Phillips and Curry to remove all 300 corbels and install new. These were moulded and manufactured from eco-friendly Jesmonite which is identical in appearance to the original Roman cement but is a more stable casting compound.

For a birds eye view of the project, CLICK ON the link below to watch the drone video

Philips and Curry director Michael Curry, a heritage roofer by trade, said:

“The roofing itself was straightforward. What was challenging was the long duration of time required in between stripping the roofs and then recovering them, which was approximately four months due to structural repairs to the roof structure and that all the new cast corbels needed to be fitted before the fascia boards could be fixed. It was a challenge keeping the building dry with temporary tarpaulins.”

He added:

“The Ffestiniog slates were great to lay. We are immensely proud of our heritage roofers for completing this exacting work and two weeks ahead of programme.”

Further structural work is required to its interior subject to further grant funding being available but, in the meantime, the Cambrian Heritage Railways have started their summer programme.

Shropshire Council has said it will be working to determine a long-term use for the building, with a scheme of internal improvements to bring the building up to a rentable standard.

Its senior project management officer Peter Gilbertson said:

“We’re so pleased that the scaffolding is finally coming down, and in time for Easter. This building holds significant cultural value for our community, and these essential repairs ensure it remains safe and usable for future generations.

“Since taking on the ownership of the building in 2023 lots of progress has been made. Whilst the scaffolding was in place we made some of the more fragile parts of the building safe, while retaining and reinstating its historic features where necessary. It really is a beautiful building and we’re proud to be involved in securing its future.”

https://buildingspecifier.com/wp-content/uploads/2025/09/WELSH-SLATE-18.09.25.jpg320800Lynhttps://buildingspecifier.com/wp-content/uploads/2019/06/building-specifier-logo.pngLyn2025-09-17 13:45:052025-09-17 13:45:07Welsh Slate helps a station building whose life was on the line

Tom Copley, Deputy Mayor of London for housing and residential development

London’s failure to build even a third of the affordable homes it is meant to is down to the Building Safety Regulator (BSR) and former housing secretary Michael Gove, according to the capital’s deputy mayor for housing.

Tom Copley said the way the BSR – which regulates the construction of higher-risk buildings – was set up has led to “unacceptable” delays in building, partly due to its capacity and partly because of its interpretation of new post-Grenfell building safety regulations, he claims.

Work has only started on 5,535 affordable homes in London since 2021 – less than a third of City Hall’s target of 17,800 by 2026.

However, Copley said he was still “very confident” the mayor would hit the target – which was downgraded last year following an agreement with the Ministry of Housing, Communities and Local Government (MHCLG) – and anticipated a “surge” in starts towards the end of this year.

He told the London Assembly housing committee:

“We are in an enormously challenging economic context, with some factors affecting London specifically.

“These include record material costs partly due to the war in Ukraine, increased labour costs due to Brexit, and 14 years of disinterest in affordable and social housing from the last government, and in the social housing sector in general.

“High interest rates have affected both supply, in terms of the cost of borrowing, and buyers, in terms of mortgage costs.

“Developing flats is more expensive and uncertain than houses – that has been affected particularly by high interest rates. Flat development in London makes up 96 per cent of our new homes compared to 17% in the rest of the country.

“While the mayor supports the principle of the BSR, the way it was set up by the previous government has led to absolutely unacceptable delays. This government has begun the process of reforming the BSR so we do expect that to improve.”

Last month Sir Sadiq Khan came under fire for his record after new figures revealed that just 347 new affordable homes were started between April and June this year.

The mayor has taken aim at the BSR as a primary factor in the lack of spades in the ground, saying last week that the “regulator hasn’t been fit for purpose”.

Copley told the committee:

“The BSR doesn’t have the capacity necessary to operate. The way the BSR has interpreted regulations has not been particularly helpful and I am very hopeful that the new leadership are going to be able to make the necessary changes.”

A BSR spokesperson told the LDRS:

“We don’t recognise this interpretation of our approach to enforcing regulation aimed at avoiding another tragedy like Grenfell.

“Most of the delays have been caused by developers failing to demonstrate their plans comply with longstanding regulations.

“We are working hard to speed up our processes while supporting industry to understand what they need to do. Ultimately, it is for developers to show their plans are safe, and already we are seeing more of them doing so successfully.”

In June, the MHCLG unveiled a new package of reforms for the BSR and appointed Andy Roe to help “evolve and improve” practices.

Sources at the Health and Safety Executive, which established the BSR in 2022, told the LDRS:

“The most significant cause of delays right now is the quality of applications from developers. However, around 70% of applications fail to do this and are therefore rejected.

“We accept the enforcement of building control standards by BSR has delayed some higher-risk building approvals. However, not enforcing the law risks the safety of residents in high-rise buildings. The purpose of the Building Safety Act, 2022 is to prevent the failures that led to the Grenfell tragedy ever happening again.”

Copley also suggested Gove’s delay in signing off the Affordable Homes Programme for London meant the capital was playing catch up.

The former Tory Housing Secretary did not rubber stamp the scheme until July 2023, with City Hall saying that work could not start on the new wave of affordable homes until later that year.

“We have had just 18 months,” Copley told assembly members. “For circumstances out of the mayor’s control and due to the previous housing sec, the [housebuilding] figure is not higher.”

Despite the issues, Copley said he was bullish on London’s future when it came to building affordable homes.

He claimed there will be the “usual hockey stick effect” – a sudden, sharp increase – in the final quarter of 2025 “because there is a very strong incentive for partners to meet the deadline in order to access funding”.

In July, the MHCLG announced that London will receive up to £11.7billion over ten years, 30% of the total national fund, to invest in building new homes for families on lower incomes.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.